Why Your 2025 Crypto Trades are Triggering New IRS Forms in 2026

Intelligence Bureau

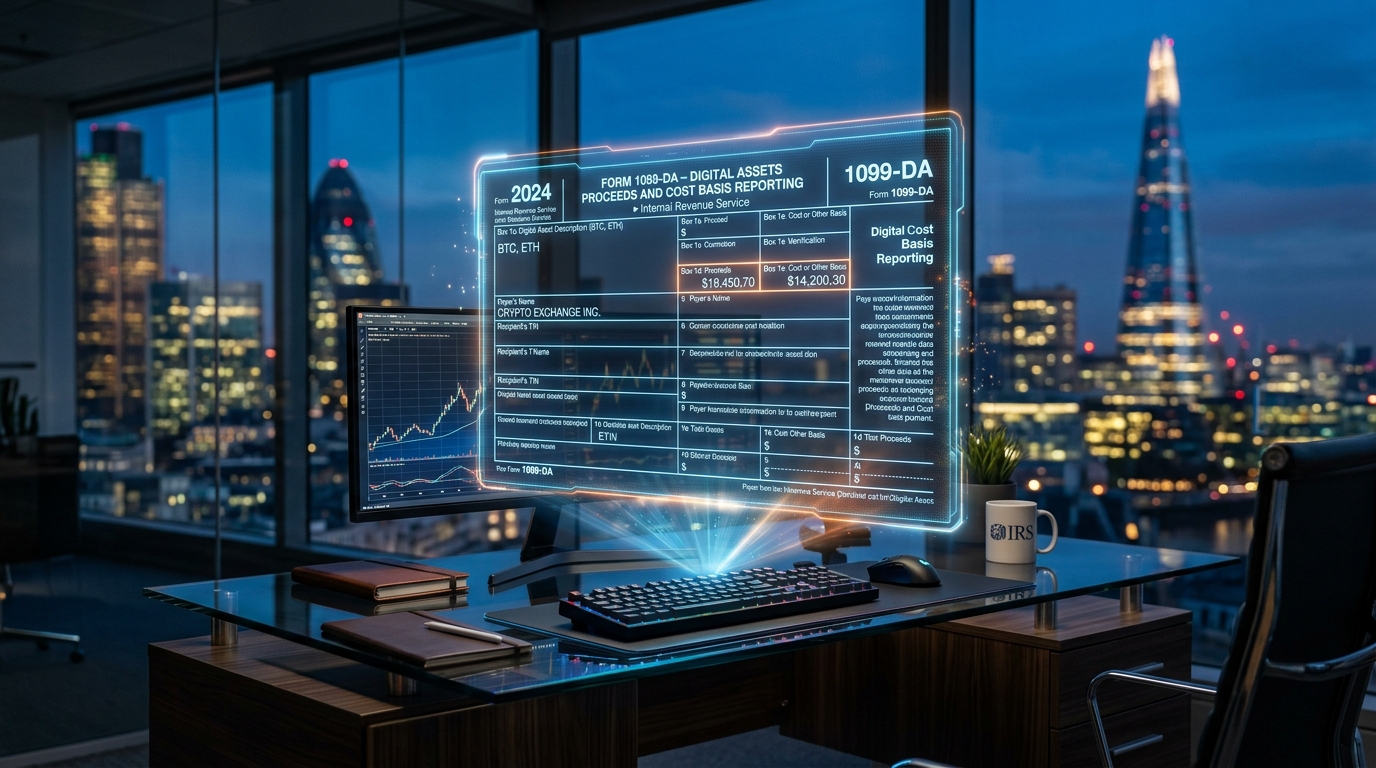

As the April 15, 2026, tax deadline approaches, U.S. cryptocurrency investors are facing the most significant shift in digital asset regulation since the inception of Bitcoin. This year marks the official debut of IRS Form 1099-DA, a dedicated information return designed specifically for "Digital Asset Proceeds From Broker Transactions." For the first time, major exchanges like Coinbase, Kraken, and Binance.US are required to report your transaction activity directly to the IRS, effectively ending the era of "voluntary" reporting.

The implementation of these rules, born from the 2021 Infrastructure Investment and Jobs Act, means that the IRS now possesses a massive database of third-party data to match against individual tax returns. While the agency has offered some "good faith" penalty relief for the 2025 tax year (reported in 2026), the burden of proof regarding cost basis—the original price paid for an asset—remains firmly on the taxpayer's shoulders.

Understanding the nuances of these new requirements is no longer optional for anyone interacting with the blockchain. From "wallet-by-wallet" accounting to new aggregate reporting thresholds for stablecoins, the 2026 tax season is a trial by fire for the crypto industry's integration into the traditional financial system.

🌍 GLOBAL MARKET IMPACT

The rollout of Form 1099-DA has sent ripples through the global crypto ecosystem, as the United States sets a high bar for tax transparency. In the EU, regulators are watching closely, with many expecting the upcoming CARF (Crypto-Asset Reporting Framework) to mirror the American approach.

Regionally, the impact is twofold:

Institutional Confidence: While retail investors may find the new rules burdensome, institutional players in the US and Europe view the standardization as a sign of market maturity. The ability to treat crypto like traditional stocks (Form 1099-B) simplifies corporate treasury audits.

Exchange Flight: Conversely, early data suggests a slight migration of "privacy-seeking" volume toward non-custodial and international exchanges. However, with the IRS successfully deploying "John Doe" summonses to offshore platforms in late 2025, the reach of US tax law is proving to be borderless.

🧠 ANALYST INSIGHT

Tax experts note that the 2026 season is "Year Zero" for automated compliance. "The IRS is no longer asking if you have crypto; they're telling you how much you sold it for," says a lead tax strategist. "The danger zone for 2026 isn't the 'gross proceeds'—the exchanges report those accurately. The danger is the missing cost basis. If you moved funds from a private wallet to an exchange, the exchange might report a $0 basis, leaving you to pay taxes on 100% of the sale price unless you have the documentation to prove otherwise."

⚠️ RISK FACTORS

Retroactive Forensic Accounting: Many investors will be forced to reconstruct transaction histories from 2021-2024 to prove their cost basis for sales made in 2025.

The "Broker" Definition: While custodial exchanges are clearly included, the 2026 season still leaves questions about "DeFi front-ends." Although the current administration has signaled a repeal of "DeFi broker" rules, the legal landscape remains volatile.

Audit Red Flags: Significant discrepancies between the 1099-DA forms received by the IRS and the amounts reported on Form 8949 will likely trigger automated underreporter notices (CP2000).

🔮 NEXT 24-HOUR OUTLOOK

In the immediate term, expect a spike in "tax-related" volatility as investors finalize their filings. We anticipate:

Liquidity Pullbacks: Increased sell pressure as retail users liquidate small portions of their portfolios to cover tax liabilities.

DEX Rotation: A short-term volume shift toward decentralized exchanges (DEXs) like Uniswap as users test the boundaries of "non-custodial" reporting before the next regulatory update.

📈 KEY TAKEAWAYS

Standardization: Crypto is now treated like stocks for reporting purposes via Form 1099-DA.

The Basis Burden: Exchanges only report what you sold for; you must prove what you paid.

Wallet-by-Wallet: You can no longer "lump" all your Bitcoin together; cost basis must be tracked per exchange or wallet.

Taxable Events: Swapping BTC for ETH, paying for coffee with DOGE, and receiving staking rewards are all still taxable events.

Advertisement

728×90 Leaderboard